-

8 Tips For Finding Yuir New Home

A solid game plan can help you narrow your homebuying search to find the best home for you. Read

Visit houselogic.com for more articles like this.

Copyright 2018 NATIONAL ASSOCIATION OF REALTORS®

By Clark Kendus

A solid game plan can help you narrow your homebuying search to find the best home for you. Read

Visit houselogic.com for more articles like this.

Copyright 2018 NATIONAL ASSOCIATION OF REALTORS®

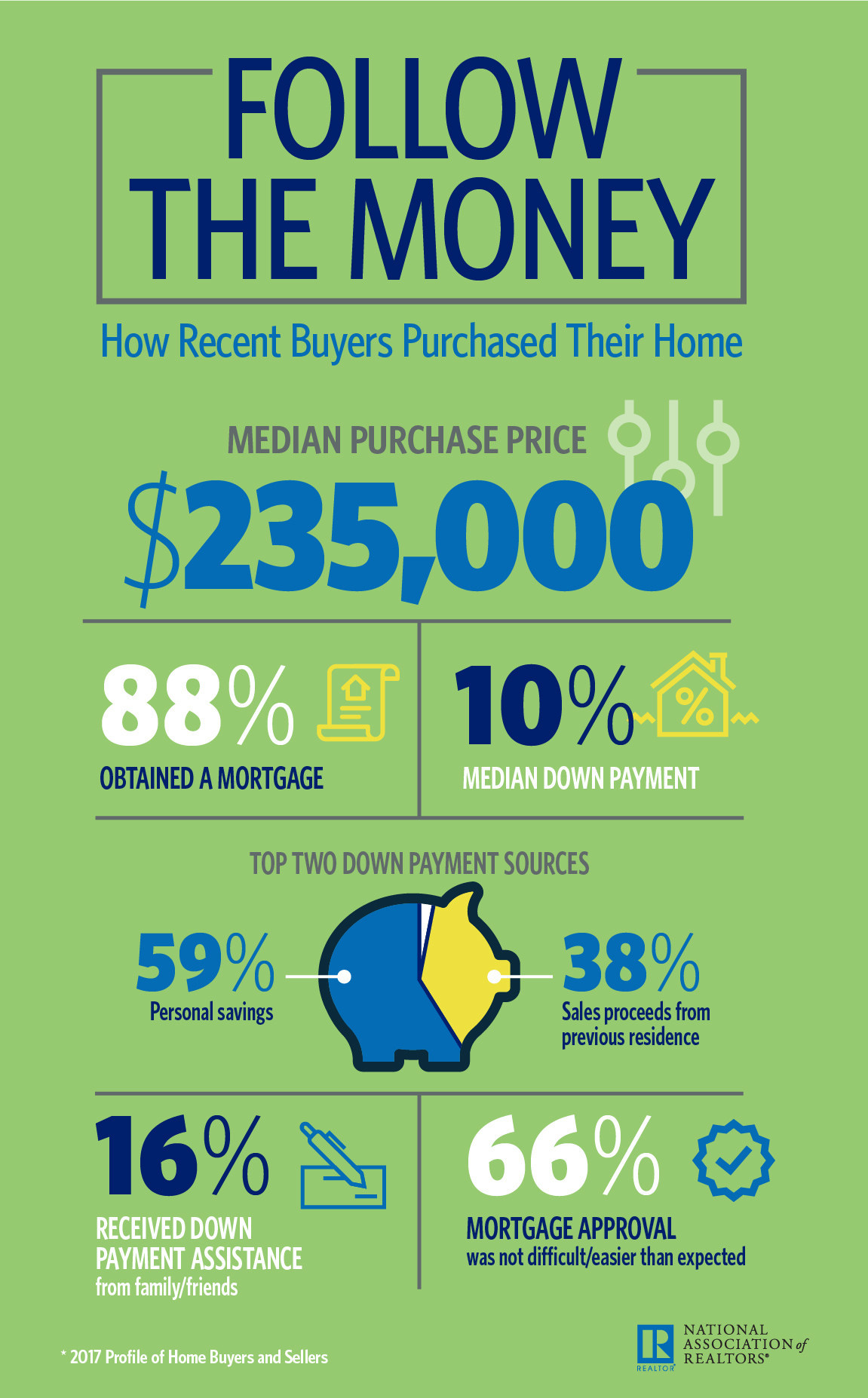

The following infographic is derived from the National Association Of Realtors (NAR) 2017 Profile Of Home Buyers And Sellers.

The profile also highlighted the following buyer and home characteristics:

Wallingford PA Real Estate – Wallingford, PA 19086

Proper preparation is key if you are planning to buy a house in 2018. Start with these steps in order to get your finances in shape.

Probably the most important step you need to undertake is to do a credit check up. If you have not checked your credit report in the past year, you definitely want to take a look now. You are entitled to receive three free credit reports a year, one from each of the main credit-reporting bureaus, on AnnualCreditReport.com. Make sure that all of the loans and accounts listed under your name actually belong to you and that the account balances are accurate. It can take several months to have an error removed from your credit report. So the earlier you look, the more time you give yourself to fix the problem before you start applying for loans.

A credit score is a numerical representation of your credit report. FICO scores range from 300 to 850, and the higher your score, the better. You will get the best interest rate on a loan if your score is 740 and above and a higher credit score should net you a lower mortgage rate.

Pay your bills on time, since payment history is the primary factor that goes into a person’s FICO score. It also helps to bring down the balances on credit cards to below 30% of the available credit.

Make sure you have enough credit. Conventional loans require at least three credit tradelines -any combination of credit cards, student loans, car loans – that have been active within the past 12-24 months. FHA loans require two tradelines. It is fine to have more, but if you have fewer, you will find it difficult to obtain a mortgage.

Resist the urge to take credit card companies up on the latest low interest deals. Opening new credit may hurt your chances of getting a mortgage, or at least of getting the best rate on a loan. By opening additional lines you can change the change your credit score and it could jeopardize your shot at getting the best interest rates on your loan.

Tighten your spending in the months before you apply for the mortgage so that you can have as much cash available as possible for your purchase. Do not purchase big ticket items in the months leading up to the start of your home search. Do not overspend on during the Holiday shopping season and squelch your impulse purchases.

You will need money for a down payment, closing costs, lender application fess, and a host of other costs. Beef up your cash reserves over the next several months. Instead of asking for gifts for the holidays suggest cash that can be put toward your new home. Getting a year end bonus? Earmark that for your home purchase too, along with any tax refund that you might be getting.

Get any cash that you may have on hand into your bank account at least 3 months prior to applying for a mortgage. Lenders will want a paper trail for any money that is deposited into your accounts that is not derived from your normal means of income. Unexpected cash appearing in accounts during your application process can be a loan killer.

If you are expecting any gifts that will be used for your home purchase get them into your accounts ahead of time. This will eliminate the need to go through the documentation process required for gifts.

Start researching mortgage lenders. Ask friends and family for any lender references that they may be able to give. If you have a bank you have been with for years try them as well. Your real estate can also be a source of lenders for you. Compare lenders against each other. Look at what they offer, costs, points, and how long to close. Also inquire to their availability to you during the process and whether or not they will attend your closing.

You should prepare your financial documents that you will need several months in advance of the actual purchase. This is a list of the documentation that you will to apply for a mortgage:

– Tax returns for the past two years

– W-2 forms for the past two years

– Paycheck stubs from the past few months

– Proof of mortgage or rent payments for the past year

– An accounting of all of your debts, including credit cards, student loans, auto loans, and alimony

– An accounting of all your assets, including bank statements, auto titles, real estate, and any investment accounts

Wallingford PA Real Estate – Wallingford, PA 19086

![]()

FHA loans present a viable borrowing alternative to conventional loans for potential home buyers. Congress established the FHA in 1934 during the Great Depression as a way for lower income borrowers to purchase a home. The FHA became part of the Department Of Housing And Urban Development in 1965. FHA loans are mortgages insured by the Federal Housing Administration (FHA). The FHA is not a lender, but an insurer. Because of their relaxed restrictions, they can sometimes offer borrowers a path to home ownership that a conventional loan may not.

When looking at loans, you may want to consider an FHA loan to avoid the more stringent requirements that often come with conventional mortgages. Since the FHA insures the loan lenders are able to loosen the qualification requirements since they are no taking on the risks associated with a borrower defaulting. A conventional lender will demand a higher credit score, larger cash down payment, and a lower debt to income ratio.

You should consider a FHA loan if:

You Have Less Than A 5% Down Payment

FHA loans require as little as 3.5% down.

Your Credit Score Is Less Than Perfect

If your credit score is less that 620 an FHA loan may be the most viable option for you. In some cases lenders will consider a credit score as low as 580. If your credit score is below 580 a 10% down payment is required.

You Are Funding Your Down Payment Entirely Via Gifted Funds

FHA guidelines allow for 100% of your down payment to be gifted. Conventional loans cap the amount of gift money that can be used as a down payment.

Your Debt To Income Ratio Is High

Your debt to income ratio (DTI) is a major determining factor in how much you can borrow. DTI is the sum of all of of your monthly debt payments divided by your monthly income. The FHA is much more lenient on maximum DTI ratios. The DTI for an FHA loan is typically 45%, but can be as high as 50% in some cases. Conventional DTI ratios carry a DTI maximum of 43%.

You Have Had A Foreclosure Or Short Sale In Your History

FHA guidelines are much more lenient than conventional loans with respect to the waiting time prior to applying for a loan following a foreclosure, short sale, or deed in lieu of foreclosure by a potential borrower. The period following the discharge of a foreclosure and a new FHA application can be as little as 3 years as opposed to 7 years for a conventional loan.

Wallingford PA Real Estate – Wallingford, PA 19086

Fences Can Define Property Lines – But Are Often Incorrectly Placed

Where is the property line? It is a question that every prospective buyer asks. The seller may answer definitively that they know exactly where the line is, and when questioned further they will cite an answer from the previous owner or on information that the neighbors have relayed. They probably have a rough idea but cannot say with absolute authority where the property lines fall, nor should you. If you are really lucky it might be possible to uncover the metal pins or small concrete markers that mark the property boundaries, but for many older homes this evidence of demarcation has long since disappeared.

The only way of knowing with certainty where your property lines are is to have a survey performed by a licensed surveyor. The cost of which usually runs about $800. A surveyed plan will mark all boundaries and lot lines along with all structures, easements and also show any potential problems.

A survey is accurate with in a fraction of an inch and will usually mark all corners for the person ordering the survey. A typical marker today is an orange stake driven into the ground. In the past a marker could have been a rock or stone marker.

The Agreement of Sale allows gives the buyer the option of electing to perform a survey as part of their due diligence, but a survey is not required when a house is sold in Pennsylvania. It seems a bit counterintuitive but when you purchase a home in Pennsylvania you do not definitively know the boundaries of the real property you are buying lie.

When is a survey necessary?

– The construction of any new features or structures on your property – a new fence, shed, garage, driveways, pools, etc. A survey is required to ensure the proposed construction does not violate any regulations regarding setbacks, etc.

– When the footprint of a home is being expanded via an addition

– The subdivision of an plot of land

– When a boundary dispute between neighbors arise

Wallingford PA Real Estate – Wallingford, PA 19086

![]()